Credit Score Chart

Friday, Jan 8 2021

There are several credit score models but for more than 25 years FICO® scores have been the industry standard for determining a person’s credit risk. The FICO® credit score chart provides a three-digit number ranging from 300 to 850 that has a lot of impact on your ability to get loans, obtain favorable interest rates, and access credit.

More than 90 percent of lending institutions use the FICO® credit score chart as a reflection of your likelihood to pay your bills on time. A low credit score indicates that you are a higher risk of not paying your debts, while a good credit score is an indicator to a lender that you’re less of a risk.

Do you know how to get a perfect credit score?

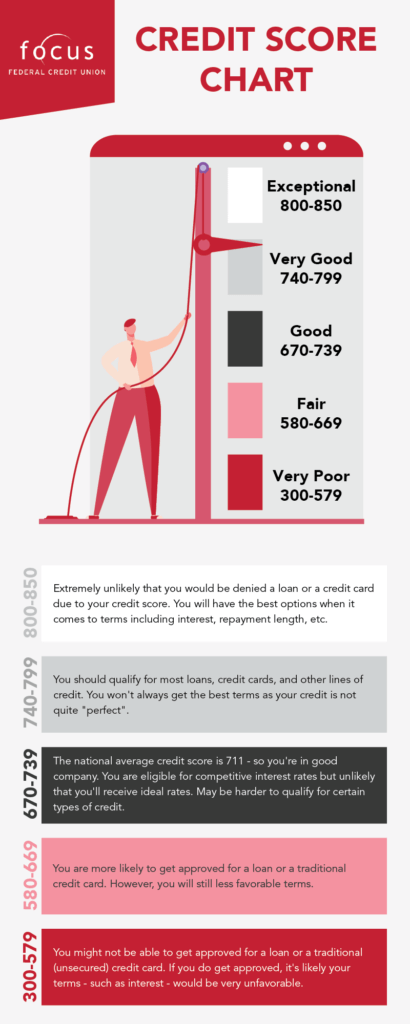

What is a Credit Score Chart?

The FICO® credit score chart shows ranges that correlate with the likelihood a person is to pay back their debt(s). Ranges are:

What factors affect your credit score?

FICO® weighs five primary factors to determine your credit score and where it falls on the credit score chart.

1. Payment History

Your payment history, the single largest credit factor, accounts for 35 percent of your score. This factors your payment history on credit cards, mortgage loans, retail accounts (department store credit cards), finance company accounts, and installment loans (such as auto loans). Negative factors such as late and missed payments, bankruptcies, lawsuits, and wage attachments can negatively impact your score, some for up to seven years.

Ways to Improve Your Payment History

- Pay your bills on time. Paying bills late, more than 30 days, can impact this portion of your score. Be sure to make at least the minimum payment on time. If you struggle with due dates, try asking creditors to move your payment dates to align with when you receive your paycheck.

- Stay current. The older a credit issue the less likely it will negatively affect your score. This means even if you had a history of late payments if you stay current your score will steadily improve.

- Look for help. Talk to your credit card companies to find out if they would be willing to lower your interest rate so that you can pay your debt sooner. Plan a budget and stick to it.

2. Credit Utilization

The second-largest factor calculated into your credit score is your credit utilization which attributes 30 percent of your score. Credit utilization measures how much credit you have access to at any given period.

You can calculate your credit utilization by adding all your credit balances and dividing that number by the total of your limits. Most experts recommend keeping your overall credit card utilization below 30 percent.

Ways to Improve Your Credit Utilization

- Make multiple credit card payments per month. Credit activity is reported monthly to the credit bureau. If you pay part or all of your credit card bill before the report is sent you can lower your credit utilization.

- Increase your available credit. If you have experienced an increase in your income you can ask your credit card company to raise your credit limit. This will in turn decrease the amount of credit you are utilizing.

- Leave your credit card accounts open. If you have paid off your balance and are no longer using your credit card, unless you are charged a fee, you should keep the account open. This shows that you have access to credit that you aren’t using.

3. Length of Credit History

Fifteen percent of your FICO® score is based on the length of your credit history. An account needs to be opened for a minimum of six months to be considered. If you just opened an account, you may not have enough credit history to calculate a score yet.

The length of your credit history accounts for 15 percent of your FICO® score. A longer credit history demonstrates that you have experience using credit.

Ways to Improve Your Credit History

- The challenge with improving your credit history is that it takes time. Leave your credit card account open even if you aren’t using them.

- Fix any credit report errors. Annually you can have your credit report pulled at no charge by Equifax, Experian, or TransUnion to check your credit. If you find an error, contact the credit bureau to have it fixed.

- Become an authorized user. If you have a family member that has a high credit score and long account history as credit, ask if you can become an authorized user on their account. This will positively impact your credit score.

4. Mix of Credit Types

A mix of credit, accounting for 10 percent of your FICO® score, considers revolving accounts, installation accounts, and open accounts. Installation accounts include loans such as auto loans, home mortgages, student loans, and home equity loans.

A revolving account would be those that have different monthly payments and would include credit cards issued by banks, retail stores, or credit unions. The final type of credit is an open account. These are a hybrid of installation and revolving credit. Examples of open accounts are gas or electric accounts.

Ways to Improve Your Mix of Credit Type

- Apply for a credit card. If you don’t currently have a credit card, consider opening one that you keep active. If you have a poor credit history, you may need to open a secured credit card to get started.

- Get an installment loan. A small car or personal loan that you can pay off quickly can help boost your credit mix.

5. Recent Applications

If you apply for a credit card or other loan the lender will pull your credit, this is considered a hard credit inquiry. Usually, hard inquiries lower your score but only by a few points. Recent applications make up 10 percent of your FICO® score.

Ways to Improve Your Recent Applications

- Reduce the number of hard inquiries. Having multiple applications over a short period of time can impact your score significantly so try to reduce the number of inquiries.

- Spread out credit applications. Credit inquiries within the past 12 months are calculated into your credit score. However, after 24 months these inquiries fall off.

Whether you’re just starting to build your credit or you need help getting over some prior credit bumps Focus Federal is here to help.

Read more about Financial Education

What’s an Ideal Credit Score?

What Is an Unsecured Loan? Everything You Need To Know Before You Borrow

Build Better Money Habits: Practical Tips You Can Actually Stick With in the New Year